You open your phone.

A notification appears: “3% cashback received.”

It looks small. Almost irrelevant.

But then you start thinking…

What if every expense — groceries, fuel, subscriptions, travel — was quietly converting into crypto?

That’s where the Binance Card cashback system becomes something much bigger than a simple reward.

It’s not just spending.

It’s a hidden accumulation strategy.

And most people misunderstand how much they’re actually earning — or worse, how much they’re losing through spreads and structure.

In this guide, I’ll break down:

- How Binance Card cashback really works

- How much you earn per $1,000 spent

- What affects your real yield

- And how to turn this into a passive crypto accumulation engine

💳 What Is Binance Card Cashback?

The Binance Card allows you to spend crypto (or converted crypto) using traditional payment rails like Visa/Mastercard.

But the real hook is:

👉 Cashback paid in crypto (usually BNB)

Instead of points or miles, you receive:

- Real assets

- With potential appreciation

- That compound over time

📊 Cashback Rates (Reality Check)

| Tier | BNB Holdings | Cashback |

|---|---|---|

| Level 1 | 0 BNB | ~0.1% |

| Level 2 | 1 BNB | ~2% |

| Level 3+ | Higher BNB | up to ~3% |

⚠️ Important:

Most users are NOT at 3%.

The average user is between 0.1% and 2%.

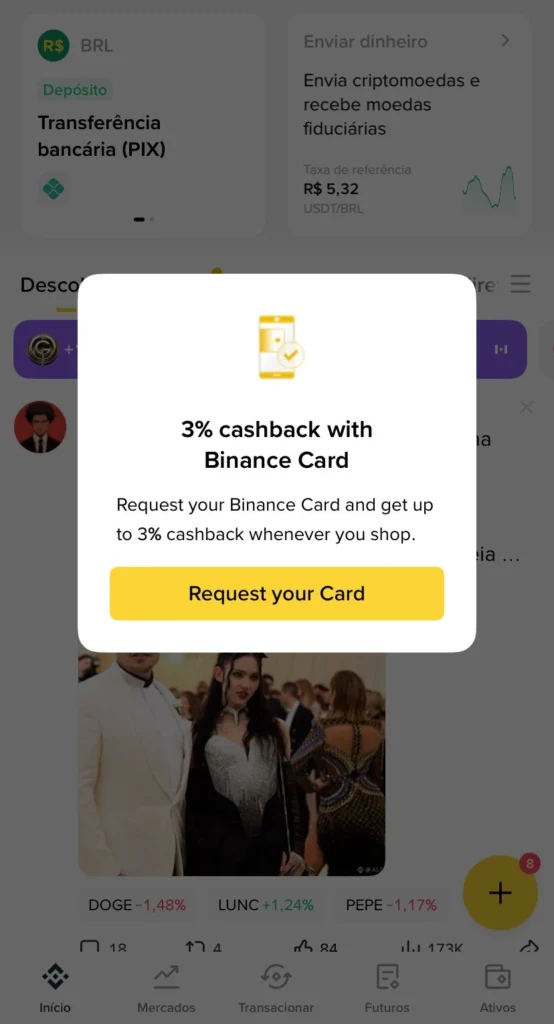

💡 The Moment You Realize You’re Leaving Money on the Table

You’re just scrolling.

Checking prices. Maybe looking at BTC, maybe USDT.

Nothing special.

Then it appears.

A small notification:

“3% cashback with Binance Card.”

At first, it feels like just another promotion.

But then something shifts.

Because you realize…

Every transaction you’ve made before —

every coffee, every subscription, every bill —

👉 generated zero return

And now suddenly, the rules are different.

Now:

- Spending becomes accumulation

- Payments become yield

- Daily life becomes a financial strategy

This is the exact moment where most users transition from:

👉 passive consumers

to

👉 active capital allocators

And that’s the real power of crypto debit cards.

Not the cashback itself.

But the change in behavior.

💰 Simulation: How Much You Earn per $1,000

Scenario 1 — Basic User (0.1%)

- Spend: $1,000

- Cashback: $1

That’s basically nothing.

Scenario 2 — Intermediate (2%)

- Spend: $1,000

- Cashback: $20

Now it starts to matter.

Scenario 3 — Advanced (3%)

- Spend: $1,000

- Cashback: $30

At scale, this becomes powerful.

📈 Monthly and Yearly Projection

| Monthly Spend | Cashback 2% | Cashback 3% |

|---|---|---|

| $1,000 | $20 | $30 |

| $3,000 | $60 | $90 |

| $5,000 | $100 | $150 |

Yearly:

- $5,000/month → $60,000/year

- Cashback 3% → $1,800/year in crypto

🧠 The Hidden Layer Most People Miss

Cashback is NOT the full story.

Because:

👉 You’re receiving crypto

Which means:

- If BNB appreciates → your cashback multiplies

- If you hold → compounding effect

- If you reinvest → exponential growth

This turns:

👉 Cashback → into DCA

🔄 Cashback as a DCA Engine

Instead of buying manually:

- You spend normally

- Cashback accumulates automatically

- You build a position without effort

This is one of the cleanest forms of:

👉 Passive accumulation

⚠️ The Real Cost (Important)

Here’s where most people lose money:

1. Spread (invisible fee)

Crypto → Fiat conversion is not perfect.

You might lose:

- 0.5% to 1.5% per transaction

2. Network choice

If you fund poorly:

- High fees eat cashback

- Wrong network kills efficiency

3. BNB exposure

To unlock higher cashback:

- You must hold BNB

- Which adds volatility risk

📊 Real Net Cashback (After Costs)

| Cashback | Spread Loss | Real Gain |

|---|---|---|

| 3% | 1% | ~2% |

| 2% | 1% | ~1% |

| 0.1% | 1% | NEGATIVE |

👉 This is why beginners often lose money.

🧠 Strategy: How to Maximize Cashback

✔️ 1. Stay at efficient tier (2–3%)

Avoid low tiers.

✔️ 2. Use low-fee networks (TRON / Solana)

Reduces friction.

✔️ 3. Treat cashback as long-term hold

Don’t sell immediately.

✔️ 4. Combine with DCA strategy

Cashback + manual accumulation = powerful combo

📦 Cluster

👉 Want to understand the full ecosystem?

- 🔗 Crypto Debit Cards Full Guide

https://damadefi.com/crypto-debit-cards-usdt-usdc-bitcoin-visa-mastercard/ - 🔗 Binance Card Full Review

https://damadefi.com/binance-card-review-2026-fees-cashback-and-hidden-costs/ - 🔗 Binance Card Fees Explained

https://damadefi.com/binance-card-fees-2026-binance-card-fees-2026/

🔮 Future: Cashback as Financial Behavior Shift

We are moving from:

- Spending → Losing money

To:

- Spending → Accumulating assets

This is subtle.

But powerful.

🧠 Final Insight

The Binance Card is not about cashback.

It’s about:

👉 Turning your daily life into a crypto accumulation system

Quiet. Automatic. Consistent.

And that’s where asymmetry lives.

❓ FAQ

1. Is Binance Card cashback really worth it?

Yes, if you are in higher tiers and control fees.

2. What crypto is cashback paid in?

Usually BNB.

3. Can cashback lose value?

Yes, due to crypto volatility.

4. Is 3% cashback realistic?

Only for users holding enough BNB.

5. What is the minimum cashback?

Around 0.1%.

6. Does Binance charge hidden fees?

Mostly via spread.

7. Can I use USDT directly?

Yes, but it gets converted.

8. Which network is best?

TRON and Solana are cheapest.

9. Can I withdraw cashback?

Yes, like any crypto.

10. Is cashback taxed?

Depends on country.

11. Does cashback compound?

Yes, if held.

12. Can I lose money using the card?

Yes, if fees > cashback.

13. Is it better than credit card cashback?

Depends on crypto appreciation.

14. Is BNB required?

For higher cashback tiers, yes.

15. Can beginners use it?

Yes, but with caution.

16. Is it good for travel?

Very good for international usage.

17. Does Binance Card work worldwide?

Depends on region.

18. What is the biggest mistake?

Ignoring spread costs.

19. Can I automate cashback reinvestment?

Manually yes, automatic depends on setup.

20. Is this passive income?

Technically yes, but linked to spending.